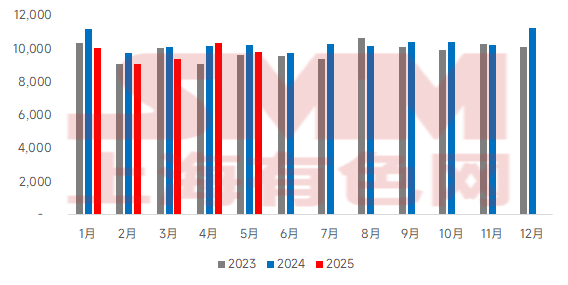

SMM, June 9, 2025: According to statistics from the General Administration of Customs of China, China imported 98.131 million mt of iron ore fines and its concentrates in May, a decrease of 5.007 million mt MoM, down 4.9% MoM, and a decrease of 3.8% YoY. The cumulative imports of iron ore fines and its concentrates from January to May reached 486.409 million mt, down 5.2% YoY.

From the perspective of SMM's port arrival data, the import volumes by country in May exhibited structural differentiation characteristics: arrivals from Australia continued to increase; however, there were significant reductions from sources such as Brazil, India, South Africa, and Ukraine. Demand side, domestic steel mills' pig iron production peaked and then pulled back, coupled with the advancement of crude steel output reduction policies, prompting some steel mills to initiate annual maintenance ahead of schedule, leading to an overall weakening of import demand. Supply side, affected by the diversion of demand to Europe and India, the proportion of Brazilian ore flowing to Europe increased, and the growth in India's domestic consumption constrained its export scale. Meanwhile, the decline in ore prices suppressed the shipping enthusiasm of non-mainstream mines such as those in South Africa, while the continuous accumulation of Ukrainian concentrate inventory at domestic ports led traders to prioritize the digestion of spot cargo, further reducing immediate purchases. Under the combined influence of multiple factors, the total iron ore imports in May showed a downward trend.

Looking ahead to June, iron ore imports are expected to increase. Despite market expectations that domestic demand will continue to decline, the decline is anticipated to be limited. Due to the continuous decline in iron ore prices, the cost-effectiveness of imported iron ore is currently higher, and steel mills have increased their usage ratio, becoming the core driving force supporting the overall high demand for imported iron ore. The supply side presents a complex situation. On the one hand, the collapse of port equipment in Peru in May will lead to a significant decline in its shipping volume. On the other hand, as the closing month of Q2, most mines will actively increase their shipping volumes to meet their mid-year production targets, a factor that will strongly drive an increase in iron ore port arrivals.

Chart-: China's Iron Ore Imports

Source: General Administration of Customs of China

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)